Toll Free:

877.456.EFSI (3374)

As traditional public-market portfolio tailwinds reverse and much of the growth engine migrates out of reach, discover why private market inclusion has become an investment imperative.

Passive 60/40 – Rise and Limitations

Passive stock/bond portfolios, with the “60/40” being the flagship, have become a cornerstone of modern investing.

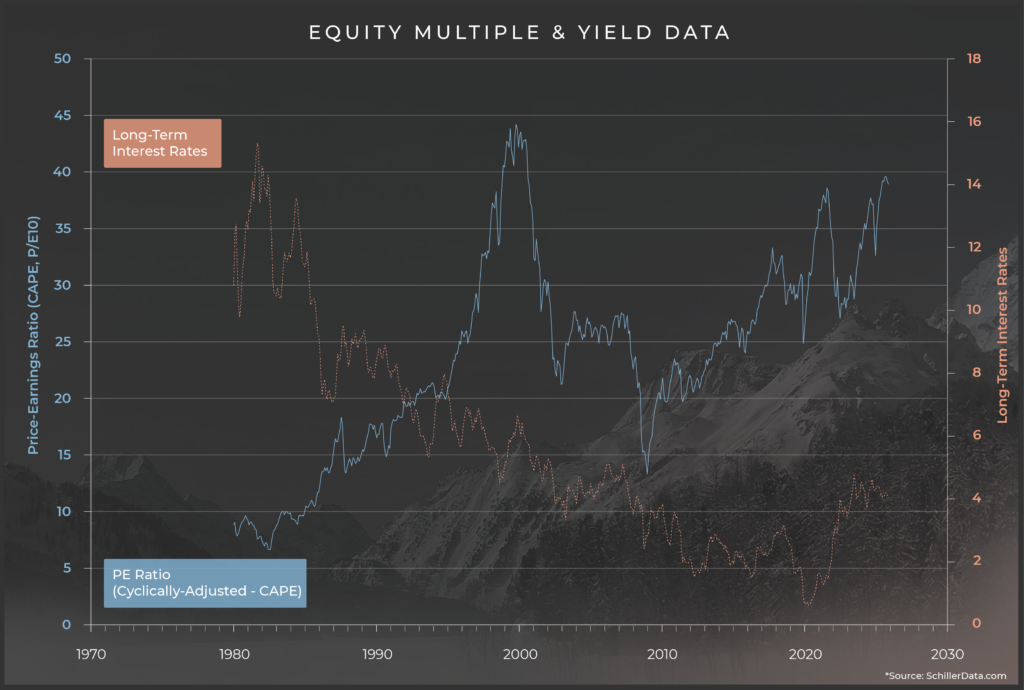

This passive risk-parity approach has delivered admirable returns over the past -40+ years. This is due in large part to high initial bond yields, as the FED hiked rates to 20% in the early ’80s to tame hyperinflation, and consequently compressed initial stock multiples. Since that time, yields have gradually trended down, allowing equity valuations to trend up… delivering tailwinds for both stock and bond asset classes for 4 decades.

Unfortunately, these tailwinds are now near their respective lower and upper bounds, presenting the mirror image of conditions that drove passive 60/40 success and flipping the tailwinds to headwinds.

Periods of high equity valuations and low real bond yields, as we have today, typically result in subsequent “lost decades” of disappointing returns.

Compounding this challenge, much of the stock market’s growth engine has migrated to private markets, leaving it inaccessible to public investors and thus passive investment vehicles. In all, we believe there is a low likelihood of passive public-market model portfolios delivering the attractive performance of past decades.

The Great Growth Migration

There has been endless debate about how to best invest in stocks: active vs. passive, growth vs. value, small cap vs. large, etc. We’d argue the overlooked question is: has the stock market itself lost relevance as an engine of wealth creation? While stocks certainly deserve a place in most portfolios, structural transformations are undermining the case for investing exclusively in public markets.

The S&P 500 story is a growth tech story, as hyper-scaling technology firms have contributed -65% of the S&P’s wealth creation since 1990. In the ’90s, over 25% of VC-funded startups eventually went public, according to a 2020 NBER study. Many startups aimed for public listings as early as possible to access growth capital necessary to scale.

Since that time, the venture capital ecosystem has exploded by more than 90X, giving growing enterprises additional funding options without the inherent burdens of being publicly-traded. Consequently, that IPO rate has plummeted to -2-3%. Not only is growth tech tapping public markets at one-tenth the rate, the median age at IPO for the firms that do go public increased from 5 years in 1999 to 12 years in 2025-well past their fastest growth years. Source: Jay R. Ritter, University of Florida, “Initial Public Offerings: Updated Statistics” (2026)

No one knows for sure what the future holds, but the trend toward a shrinking public market opportunity set is clear. The total number of US public companies has shrunk 58% from 8,800 in 1998 to 3,657 at the end of 2025. Currently, 87% of all US companies with revenues exceeding $100 million are private. In 2022-2024, take-private acquisitions exceeded new IPO fundraising by over 3.5x. As Private capital markets continue to expand, the burdens of a public listing have only grown, such as:

- Regulatory and compliance burdens draining resources and management attention.

- Disclosure requirements inherent to being public. Companies are increasingly prizing the ability to shield proprietary information.

- Quarterly earnings and guidance pressure. Private ownership enables long-term strategic focus.

- Distracting activist campaigns. Management of private companies can control the cap table.

With the dearth of fresh blood entering the public markets, the S&P 500 is concentrating into a museum of yesterday’s leaders. The “Magnificent 7” technology stocks now represent -35% of the S&P 500, and they are no longer delivering the high double or triple-digit revenue growth rates they did in their earlier years (except for Nvidia, of course).

Instead, passive investment dollars are chasing public proxies for Al exposure, stretching valuations while settling for companies with merely tangential exposure to the Al revolution. Meanwhile, pure-plays building tomorrow’s breakthroughs remain inaccessible to everyday investors.

Private Market Advantages and the Endowment Model

Institutional investors have increasingly turned to private markets as a core driver of portfolio performance.

Many of the most sophisticated endowments, foundations, and large family offices now allocate -30-70% of their assets to private markets. Nothing exemplifies this evolution more clearly than the Endowment Model, brought to life by Yale Endowment’s David Swensen and detailed in his seminal work Pioneering Portfolio Management. At the heart of Yale’s success was a heavy allocation to private market investments. According to Ted Seides’ book, Capital Allocators, Yale’s portfolio’s composition consisted of:

- -10% US Stocks, Bonds, & Cash

- -14% International Equities

- -76% Private Market Assets

Over Swensen’s 35-year tenure as CIO, Yale’s endowment posted 13.1% annualized returns, exceeding peer institutions by 3.4% and the 60/40 by 4.3%. The compounded effect of that 35-year 4.3% outperformance would result in a final portfolio value almost 4X that of the 60/40.

His success transformed institutional investing, with his model becoming the institutional blueprint and catalyzing explosive growth in private markets as allocators sought to capture its advantages, which can include:

- Enhanced Diversification

- More persistent performance dispersion for managers in the private markets than in the public markets, allowing discerning aIlocators to outperform

- IIliquidity premium adding 2-6% higher annualized returns with similar risk compared to public market equivalents.

- Reduced sequence-of-return risk

- More stable return profiles

- Asymmetric risk/return

- Principal Protection

- Structural behavioral advantages, as lower mark-to-market volatility reduces likelihood of impulsive decision-making at the wrong time, and iiliquidity prevents it

- Friction between capital and consumption, reinforcing saving & investing discipline (more for individual investors)

Implementation Considerations & Challenges

Private market inclusion introduces some complexities, such as:

- Selecting appropriate asset classes, strategies, and geographies

- Identifying and evaluating top-tier managers, who are usually outside mainstream channels

- Due diligence and ongoing monitoring of managers

- Liquidity provisioning for unpredictable capital calls while avoiding cash drag

- Complex tax administration and dozens of K-ls

There are no passive options with respect to private market investing. Effective implementation requires a professional and discerning capital allocator with institutional infrastructure. These resources are cost-prohibitive for all but the wealthiest of families.

**********

Jarrod Dean, CFA is Chief Investment Officer and Portfolio Manager at Alpenglow Private Capital. Connect with him on LinkedIn here.

*Any views expressed in this article are those of the author(s) and do not necessarily represent those of EFSI.